Key Takeaways

- Consolidating multiple credit card debts into a single loan with a lower interest rate makes managing payments easier and can save you money over time.

- Through negotiation, debt settlement can lower the total amount owed to creditors, but it may impact your credit score and take time to complete.

- Chapter 7 and Chapter 13 bankruptcy options help eliminate or restructure debt, but they have long-term effects on your credit score and may involve selling assets.

- Debt consolidation, settlement, and bankruptcy each have benefits and risks, and understanding them is key to choosing the right solution for your financial situation.

- Debt Redemption Texas Debt Relief offers debt settlement programs exclusively for Texans, often as a better alternative to bankruptcy, with fees up to 40% less than out-of-state services.

Debt Redemption Texas Debt Relief is a trusted debt relief company in Texas dedicated to helping consumers overcome their financial challenges. We offer personalized solutions including a debt settlement program exclusively offered only to Texans, a debt consolidation loan platform to shop for the best rates, and access to credit counseling solutions via our partners, to help you reduce and manage debt effectively. With a commitment to transparency and customer support, Debt Redemption Texas Debt Relief provides free consultations to guide you towards financial freedom.

As seen on Good Morning Texas, Texas Today, Great Day Houston, Great Day SA, We Are Austin and Daytime

Credit Card Debt Relief in Plano

Introduction to Debt Relief Options

In Plano, managing credit card debt can be challenging, but multiple debt relief options are available. Understanding the differences between debt consolidation, settlement, and bankruptcy is key.

What is Debt Consolidation?

Debt consolidation combines multiple debts into a single loan or repayment plan. It simplifies payments and often results in a lower interest rate, making it a popular choice for those with multiple credit card balances.

How Debt Consolidation Works

You take out a new loan to pay off existing debts, typically at a lower interest rate. This means fewer payments to manage and potential savings on interest.

For example, if you have three credit card balances totaling $10,000, you can consolidate them into one loan and make a single payment instead of three.

Types of Debt Consolidation

- Personal Loans – Unsecured loans to pay off credit card debt.

- Balance Transfer Credit Cards – Offer 0% introductory APR for transferring balances, with no interest for a limited time.

- Home Equity Loans – Use your home’s equity to consolidate debts.

Pros and Cons of Debt Consolidation

| Pros | Cons |

| Lower interest rates can save money over time. | May require good credit for the best rates. |

| Single monthly payment simplifies financial management. | Doesn’t reduce the total debt amount. |

| Timely payments can improve your credit score. | Risk of accruing more debt if spending habits don’t change. |

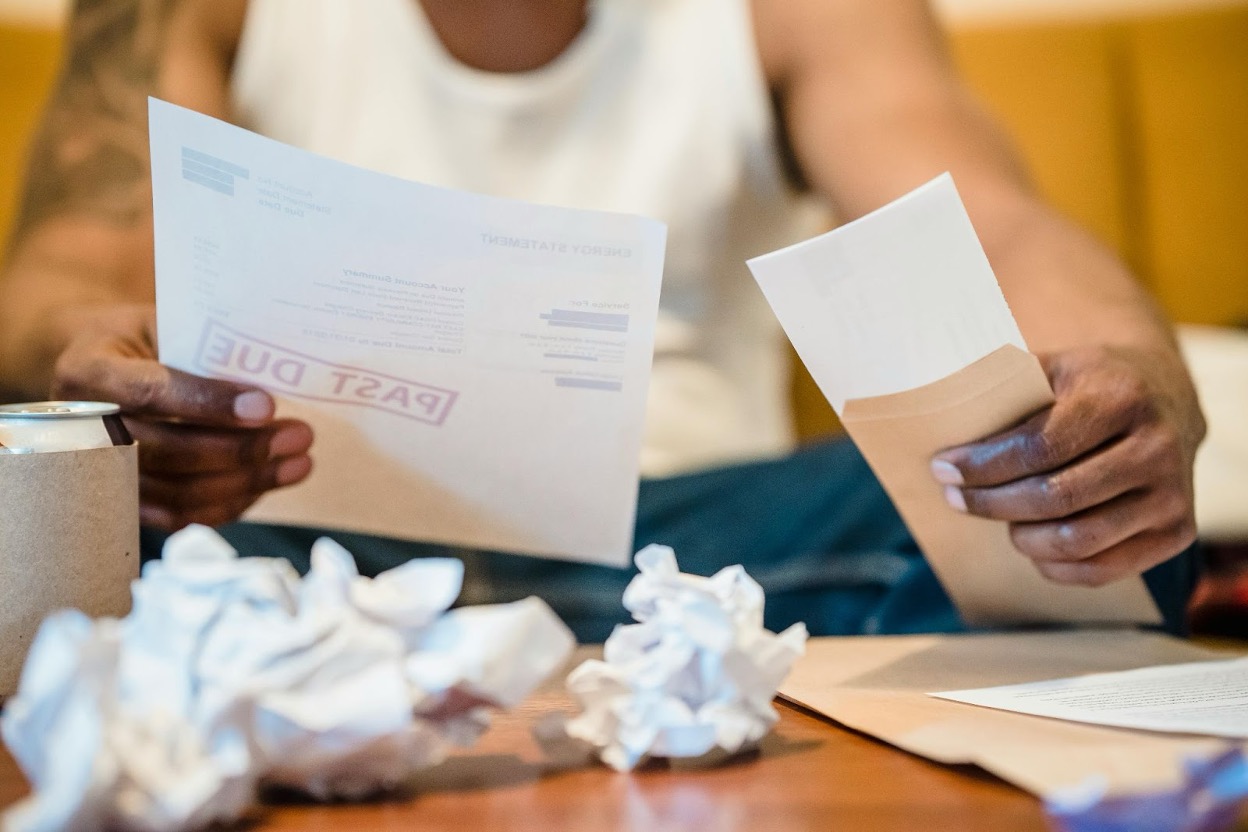

What is Debt Settlement?

How Debt Settlement Works

Debt settlement involves negotiating with creditors to pay less than the full amount owed, reducing your total debt but impacting your credit score.

For example, you owe $10,000 and negotiate to pay $6,000, with the creditor forgiving the remaining $4,000.

When to Consider Debt Settlement

- Typically considered when you can’t pay debts in full and are facing financial hardship.

- Not all creditors may agree, and the process can take time.

Pros and Cons of Debt Settlement

| Pros | Cons |

| Significant debt reduction and no accruing interest once settled | Can impact your credit score |

| Helps avoid bankruptcy | Although the vast majority of creditors settle, some creditors may not agree to settle |

| Clear path to resolving high-interest debt | Forgiven debt may be considered taxable income |

Understanding Bankruptcy

Bankruptcy allows you to eliminate or restructure debts, providing relief for those in severe financial distress. It’s often considered a last resort due to its long-term impact on credit.

Types of Bankruptcy

- Chapter 7: Also called liquidation bankruptcy, involves selling non-exempt assets to pay off debt, with remaining debt discharged. Typically completed within a few months.

- Chapter 13: Known as reorganization bankruptcy, allows you to keep assets and repay debts over three to five years, suitable for those with regular income.

Chapter 7 vs Chapter 13

- Chapter 7: Quicker but may require selling assets.

- Chapter 13: May let you keep assets but requires a longer repayment commitment.

If you need to protect equity in your home, Chapter 13 might be better. If you have limited assets and need to eliminate debt quickly, Chapter 7 may be more appropriate.

Pros and Cons of Bankruptcy

| Pros | Cons |

| Eliminates most unsecured debts | Severely impacts credit score for 7-10 |

| Chapter 7 provides a fresh financial start | May require selling assets |

| Stops collection efforts and legal actions | Bankruptcy filing becomes public record |

Determining the Best Option for Your Situation

Steps to Take for Credit Card Debt Relief

Assessing Your Financial Status

Start by listing all debts, including amounts owed, interest rates, and minimum monthly payments. Consider your income, expenses, and any assets you may have. This assessment helps you understand your debt and determine the most effective relief option.

Consulting Financial

Consulting a Debt Specialist can provide valuable insights into your options.Debt Redemption Texas Debt Relief provides free consultations to help you evaluate choices and develop a personalized plan. Professionals can help weigh the pros and cons of each option and guide you to the best solution.

Creating a Debt Relief Plan

Create a detailed debt relief plan outlining your goals, steps, and timeline for achieving them. This plan should include a budget to manage expenses and ensure necessary payments.

Implementing Your Chosen Strategy

After selecting the best debt relief option, implement your strategy effectively. Follow your structured plan and stay committed to your financial goals.

- If you’ve chosen debt consolidation, understand the terms of your new loan or repayment plan. Make timely payments and avoid additional debt. Create a budget to manage expenses and prevent future financial difficulties.

- If you’ve opted for debt settlement, work closely with your debt settlement company to negotiate with creditors. Be prepared for the possibility that some creditors may not agree to settle. Continue making minimum payments to avoid further damage to your credit.

- For those deciding on bankruptcy, follow the legal process carefully. Attend credit counseling sessions, file the necessary paperwork, and attend court hearings. Your bankruptcy attorney will guide you through each step to ensure compliance with legal requirements.

Monitoring Your Progress

Monitoring your progress ensures your debt relief strategy works effectively. Regularly review your financial situation, track payments, and adjust your plan as needed. Consider setting up automatic payments to avoid missing due dates. Additionally, monitor your credit report for changes to ensure your efforts positively impact your credit.

How Debt Redemption Texas Debt Relief Can Help

At Debt Redemption Texas Debt Relief, we specialize in providing tailored debt relief solutions exclusively for Texans. With over 20 years of experience, we understand the specific rules, regulations, and benefits that apply in Texas.

As a Texas-only debt relief company, we offer services such as debt settlement and guidance on alternatives to bankruptcy. While our services can negatively affect your credit score, depending on where they are now, they help you resolve your debt and rebuild your financial standing. We can also assist in securing a debt consolidation loan of up to $100,000 through our affiliate platform.

Our fees are up to 40% less than out-of-state debt relief services, and program payments are often less than half compared to minimum credit card payments. We’ve helped thousands of Texans since 2002, enabling them to break free from high-interest debt and gain control of their financial future.

Book your free consultation

Frequently Asked Questions (FAQ)

What is the difference between debt settlement and debt consolidation?

Debt settlement negotiates with creditors to pay less than the full amount owed, which can reduce your total debt but may hurt your credit score. Debt consolidation combines multiple debts into one loan with a lower interest rate, simplifying payments without reducing the total debt.

Will debt relief affect my credit score?

Debt consolidation has a minimal impact if managed responsibly. Debt settlement can lower your credit score since settled debts may be marked “settled in full for less than the full amount,” or similar. Bankruptcy has the most severe impact, staying on your credit report for 7-10 years.

How long does the debt consolidation process take?

The process varies depending on the type of consolidation. Personal loans and balance transfer credit cards can take a few days to weeks, while home equity loans may take longer, typically a few weeks to months due to the appraisal process.

Is bankruptcy the best option for everyone in debt?

Bankruptcy is usually a last resort for those who cannot manage their debts through other means. Before filing, consider alternatives like debt consolidation or settlement. Consulting a debt specialists can help you decide if bankruptcy is the right choice.

Can I negotiate debt settlement on my own?

Yes, but it can be challenging. Working with a company like Debt Redemption Texas Debt Relief simplifies the process and may lead to better results with creditors.

What fees are associated with debt settlement?

Debt settlement companies typically charge Texans 25% of the settled debt. Always ask for a detailed fee explanation before agreeing to any terms. Debt Redemption charges 15%, which is significantly lower than many out-of-state providers.

What are the long-term effects of debt relief?

Debt consolidation can improve your credit score if managed properly, while debt settlement and bankruptcy can have negative impacts. Weigh the pros and cons of each option and work with a financial advisor to create a plan to rebuild your credit over time. It is important to note that credit can always be established once the debt is resolved. Newer FICO scoring systems may not consider paid/settled collection in your score, so resolving these debts can have a very positive impact.